Long-term downside pressure on steel scrap and iron ore prices

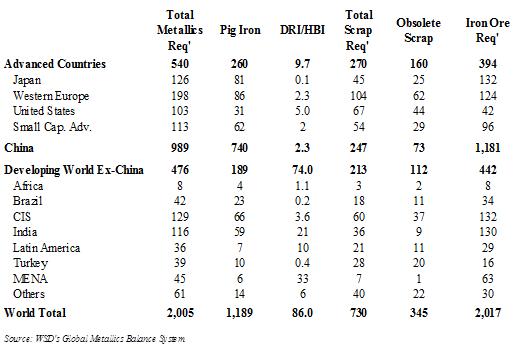

The global metallics balance for the steel and foundry industries often has as great, if not a greater, impact on HRB export prices as the steelmaking supply/demand balance. The global metallics requirement in 2016 for the steel and foundry industries will be about 2.0 billion tonnes, consisting of about 1.2 billion tonnes of pig iron, 78 million tonnes of steel scrap substitutes and 738 million tonnes of steel scrap. The steel scrap usage figure includes about 200 million tonnes of home scrap, 198 million tonnes of new scrap (largely returned by factories) and 353 million tonnes of obsolete steel scrap (of which about 75 million tonnes is generated in China). All steelmakers' metallics, and some other steel-related materials reside in the same global bathtub - including iron ore, coking coal, metallurgical coke, pig iron, steel scrap and steel scrap substitutes.

Global Metallics Summary 2016

(million metric tonne)

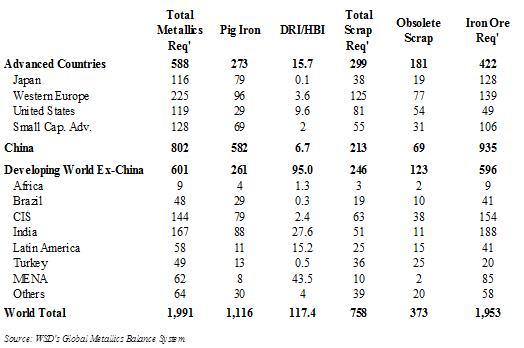

By 2025, the metallics requirement for the steel and foundry industries may be little changed from 2016 assuming that lower Chinese steel production is offset by gains principally in the Developing Countries. Versus 2016, global pig iron production may drop 74 million tonnes, or about 6%, while steel scrap substitute production may rise 31 million tonnes, or 40%.

New steel scrap generated by factories may rise to 209 million tonnes, while home scrap generation may fall 12% to 176 million tonnes.

The obsolete steel scrap requirement in 2025, at 373 million tonnes, is only 29 million tonnes higher than in 2016. Yet, the obsolete steel scrap reservoir 10-40 years old, on average. will be about 37% higher at about 580 million tonnes. On this basis, the global obsolete steel scrap recovery ratio, as a share of the scrap reservoir that's on average 10-40 years old, declines to 66% in 2025 from 86% in 2016. Such a low recovery ratio for 2025 is hard to fathom unless the price of steel scrap is so depressed that its collection is retarded. Yet, demolition projects, often go ahead no matter what the price of the steel scrap. Demolition may account for as much as 50% of the recovery of obsolete steel scrap apart from that recovered via the recycling of automobiles and appliances (often processed in shredders in the Advanced Countries).

Global Metallics Summary 2025

(million metric tonne)

What's the upshot? Looking down the road 10 years, the growing obsolete steel scrap reservoir will be a force driving down both steel scrap prices and iron ore prices; and, on balance, work to diminish the "economic rent" of integrated steelmakers.

This report includes forward-looking statements that are based on current expectations about future events and are subject to uncertainties and factors relating to operations and the business environment, all of which are difficult to predict. Although we believe that the expectations reflected in our forward-looking statements are reasonable, they can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including among other things, changes in prices, shifts in demand, variations in supply, movements in international currency, developments in technology, actions by governments and/or other factors.

The information contained in this report is based upon or derived from sources that are believed to be reliable; however, no representation is made that such information is accurate or complete in all material respects, and reliance upon such information as the basis for taking any action is neither authorized nor warranted. WSD does not solicit, and avoids receiving, non-public material information from its clients and contacts in the course of its business. The information that we publish in our reports and communicate to our clients is not based on material non-public information.

The officers, directors, employees or stockholders of World Steel Dynamics Inc. do not directly or indirectly hold securities of, or that are related to, one or more of the companies that are referred to herein. World Steel Dynamics Inc. may act as a consultant to, and/or sell its subscription services to, one or more of the companies mentioned in this report.

Copyright Ó 2016 by World Steel Dynamics Inc. all rights reserved